Are you in your 20s and ready to take control of your finances? It’s never too early to start planning for your financial future. The decisions you make now can set you up for a lifetime of financial stability and success. It’s time to start making smart money moves and set yourself up for a bright financial future.

The Exciting Importance of Financial Planning in Your 20s

Your 20s are a thrilling time of transition and growth. You’re starting your career, earning a steady income, and laying the foundation for your future. But with all these exciting changes comes the responsibility of managing your finances. It’s a decade to focus on paying off debts, building an emergency fund, and saving for your future goals. Don’t let finances stress you out – now is the time to start taking control and making the most of your money.

A Quick Peek into the 13 Smartest Money Moves

In this article, we’re going to dive into the 13 smartest money moves you can make in your 20s. Whether you’re just starting out or already well into your 20s, these tips will help you build a strong financial foundation and set you up for financial freedom. Get ready to be inspired and motivated to take your finances to the next level!

Start an Emergency Fund – The Foundation of Your Financial Future

Life is unpredictable, and having an emergency fund is essential for weathering any financial storm that comes your way. This fund will give you peace of mind, reduce financial stress, and allow you to take control of your finances.

A. Why an Emergency Fund is So Important

Unexpected events can happen at any time, and having an emergency fund will help you stay afloat during those tough times. Whether it’s a job loss, unexpected medical expenses, or a car breakdown, an emergency fund will help you avoid falling into debt and give you the financial stability you need to get back on your feet.

B. How Much to Save

Most financial experts recommend saving three to six months of living expenses in an emergency fund. This may seem like a lot, but remember that the goal is to have a safety net in case of an emergency. Start small, and gradually increase your savings each month.

C.Tips for Building an Emergency Fund

Building an emergency fund takes time and discipline, but it’s worth it. Here are some tips to help you get started:

– Set a savings goal and stick to it

– Automate your savings so you’re putting away money each month without thinking about it

– Cut back on expenses and find ways to save money

– Consider taking on a side hustle to increase your income

– Be patient and consistent, your emergency fund will grow over time

Starting an emergency fund is a smart and empowering move, and it’s never too early to start. Start today, and you’ll be well on your way to financial stability and peace of mind.

Pay Off Debt – Say Goodbye to Financial Burden

Debt can be a heavy burden, and it’s important to take control of it before it takes control of you. Whether it’s student loans, credit card debt, or any other form of debt, paying it off should be a top priority.

A. Prioritizing Debt Repayment

It’s essential to prioritize debt repayment and make a plan to pay it off as quickly as possible. Start by creating a list of all your debts, including the interest rate, minimum payment, and balance. Focus on paying off the debt with the highest interest rate first, and work your way down the list.

B. Strategies for Paying Off Debt Quickly

Getting rid of debt can feel overwhelming, but with a solid plan and some hard work, you can pay it off faster than you think. Here are some strategies to help you pay off debt quickly:

– Increase your income by taking on a side hustle or asking for a raise

– Make extra payments or increase your monthly payments

– Cut back on expenses to free up more money to put towards debt repayment

– Consider a debt consolidation loan or debt management plan

C. The Impact of Debt on Your Credit Score

Your credit score is a reflection of your financial responsibility, and having a high credit score can impact your ability to get a loan, rent an apartment, or even get a job. High levels of debt can lower your credit score, so it’s essential to pay off debt as quickly as possible to improve your credit standing.

Paying off debt can be a challenge, but it’s worth it. The quicker you pay it off, the sooner you’ll experience the freedom of financial stability and peace of mind. To inspire you, let me share a personal story about a friend of mine.

My friend, we’ll call her Sarah, was once overwhelmed by her student loan debt and credit card debt. She had accumulated over $25,000 in debt from her student loans and had been using her credit card for daily expenses, which had caused her balance to spiral out of control. But Sarah was determined to take control of her finances.

She started by making a plan. She made a list of all her debts, including the interest rate, minimum payment, and balance, and prioritized which debt to pay off first. Sarah knew she needed to increase her income, so she took on a part-time job as a freelance graphic designer in addition to her full-time job. She also made cuts to her expenses by cooking more meals at home and cutting back on entertainment expenses.

With her extra income and reduced expenses, Sarah was able to make extra payments towards her debts each month. In just two years, she was able to pay off all her debt and felt a huge weight lifted off her shoulders. She now has the peace of mind and freedom to save for her future goals.

Sarah’s story shows that paying off debt is achievable and well worth the effort. By making a plan, increasing her income, and cutting back on expenses, Sarah was able to turn her financial situation around. So, let’s make a plan and tackle that debt!

Read More: Turning Your Passion into Profit: How to Make Money from 20 Hobbies

Create a Budget

When it comes to managing your money, creating a budget is key to success. Budgeting is all about understanding your income and expenses and making a plan for your money. It’s about setting financial goals and sticking to a budget so you can reach those goals.

A. Understanding your income and expenses

Have you ever wondered where all your money goes at the end of the month? I know I have. That’s why I started creating a budget for myself. By understanding my income and expenses, I was able to see exactly where my money was going and make adjustments to my spending. I found that I was spending more money on eating out and shopping than I realized, and by cutting back in these areas, I was able to save more money each month.

B. Setting financial goals and sticking to a budget

Budgeting has played a huge role in my financial success. It has helped me to stay on track and reach my financial goals. Whether your goal is to save for a down payment on a house, pay off debt, or save for retirement, a budget is essential. It allows you to see exactly where your money is going and make adjustments as needed so you can reach your goals.

C. The role of a budget in financial success

So, let’s get started on creating a budget! Start by tracking your income and expenses for one month. Then, set a budget for each category of expenses. And most importantly, stick to your budget. By doing this, you’ll be on your way to financial success.

Read More: https://moneysmart.gov.au/budgeting/budget-planner

The Importance of Saving for Retirement

When it comes to your financial future, saving for retirement should be a top priority. Why? Because the earlier you start, the more time your money has to grow. And the more time your money has to grow, the more comfortable your retirement will be.

A. Options for Retirement Savings

When it comes to saving for retirement, there are several options available. A popular option is a 401(k) plan, which is offered by many employers. If your employer offers a 401(k) plan, consider contributing as much as you can to take advantage of any employer matching contributions. Another option is an individual retirement account (IRA). IRAs offer tax benefits and the option to choose from a variety of investment options.

B. Maximizing Contributions for Maximum Benefits

Regardless of which option you choose, the key is to start early and make regular contributions. The earlier you start, the more time your money has to grow, and the less you’ll have to save each month. So, make a plan to start contributing to your retirement savings as soon as possible and aim to increase your contributions as you receive raises or bonuses. By maximizing your contributions, you’ll be on your way to a comfortable retirement.

I remember when I first started thinking about retirement, I was in my 20s, and it seemed so far away. But time flies, and now, I’m so glad I started saving for retirement early. It’s never too early or too late to start saving for retirement, so why not start today? Your future self will thank you.

The Long-Term Benefits of Continued Education

Investing in your education is one of the smartest money moves you can make. Not only will it provide you with knowledge and skills that will serve you throughout your life, but it can also have a significant impact on your career and earning potential.

A. Options for Financing Education

Continuing your education can be expensive, but there are options available to help you finance it. Scholarships and grants can be a great way to pay for your education without having to pay it back. If you need to take out student loans, make sure to understand the terms and consider your repayment options before signing on the dotted line.

B. The Impact of Education on Career and Earning Potential

The investment you make in your education can pay off in the long run. Studies have shown that individuals with higher levels of education tend to have higher paying jobs and are less likely to be unemployed. Investing in your education can provide you with the skills and knowledge you need to advance in your career, leading to higher earning potential.

I can attest to the long-term benefits of continued education. After I finished my undergraduate degree, I went back to school to get my master’s degree. The investment I made in my education has opened doors for me that I never would have thought possible. And, my increased earning potential has allowed me to live a comfortable life and reach my financial goals.

So, whether it’s going back to school for a degree or taking a course to learn a new skill, investing in your education is a smart money move that can pay off in the long run.

The Benefits of Investing

Investing your money is a smart way to grow your wealth and secure your financial future. It’s never too early (or late) to start investing, and the earlier you begin, the more time your money has to grow.

A. Options for Investing

There are many options for investing your money, including stocks, bonds, real estate, and more. Each type of investment has its own set of risks and rewards, so it’s important to do your research and choose the options that align with your financial goals and risk tolerance.

B. Tips for Getting Started with Investing

Getting started with investing can feel overwhelming, but it doesn’t have to be. Here are a few tips to help you get started:

– Start with a small amount of money:

You don’t need a lot of money to start investing. Even small amounts can add up over time.

– Educate yourself:

Learn about the different types of investments and understand the risks and rewards associated with each one.

– Work with a financial advisor:

A financial advisor can help you create an investment strategy that aligns with your financial goals and risk tolerance.

I remember when I first started investing, I was intimidated by all the options and jargon. But, by taking it one step at a time and educating myself, I was able to build a solid investment portfolio that has helped me reach my financial goals.

So, don’t wait any longer. The earlier you get in, the more potential for growth over time.

Read More: The Pros and Cons of Different Investment Vehicles: Stocks, Bonds, and Real Estate

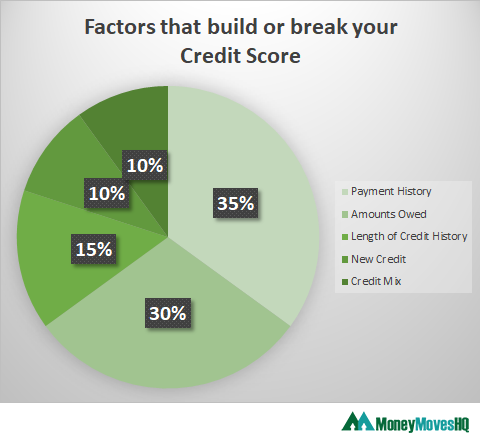

Understanding Credit and Credit Scores

Credit is a key aspect of personal finance. Your credit score, which is a numerical representation of your creditworthiness, is used by lenders to determine your risk as a borrower. It’s important to understand credit and build good credit, as it can impact your ability to secure loans for big purchases, such as a home or car, and can also affect the interest rates you are offered.

A.Strategies for Building and Maintaining Good Credit

Building good credit takes time and effort, but it’s well worth it in the long run. Here are a few strategies for building and maintaining good credit:

– Pay your bills on time:

Late payments can negatively impact your credit score. Set up automatic payments or reminders to ensure you never miss a payment.

– Keep credit card balances low:

High credit card balances can signal to lenders that you are overextended and may struggle to repay debts. Keep your balances low and make payments on time.

– Limit new credit applications:

Every time you apply for credit, it’s recorded on your credit report. Limit new credit applications and make sure to pay off any existing debt before applying for more.-

B.The Impact of Credit on Financial Stability

Good credit can have a positive impact on your financial stability. With a strong credit score, you can secure loans with lower interest rates, which can save you money in the long run. On the other hand, poor credit can limit your ability to secure loans and can result in higher interest rates, making it more difficult to achieve your financial goals.

I know from personal experience the importance of building good credit. When I first started out, I didn’t understand the impact of credit on my financial stability. But, by following the strategies above and being mindful of my credit habits, I was able to significantly improve my credit score and secure loans with better interest rates.

So, don’t underestimate the power of good credit. Start building and maintaining good credit today, and watch your financial stability improve!

Read More: Credit Cards 101: Understanding the Pros and Cons and How to Use Them Responsibly

Understanding the Different Types of Insurance

Insurance can be a confusing topic, but it’s important to understand the different types of insurance available to you. From health insurance to car insurance, each type of insurance serves a specific purpose and provides coverage for different events.

A. The Importance of Being Adequately Insured

No one likes to think about worst-case scenarios, but insurance provides a safety net in case something unexpected happens. Being adequately insured means that you are protected from financial loss in the event of an accident, illness, or other covered event. Without insurance, you could be faced with large medical bills or repair costs, which could have a major impact on your finances.

B. Tips for Finding the Right Insurance Coverage

Finding the right insurance coverage can be a challenge, but there are a few tips that can help you make the right choice:

– Assess your needs:

Consider what events you need coverage for and what risks you want to protect against.

– Compare insurance options:

Don’t settle for the first policy you come across. Shop around and compare different insurance options to find the one that best fits your needs.

– Read the fine print:

Make sure you understand the terms and conditions of each insurance policy before making a decision.

I remember when I first started thinking about insurance. I was overwhelmed by all the different options and wasn’t sure where to start. But, by taking the time to assess my needs, compare insurance options, and read the fine print, I was able to find the right coverage for me.

So, don’t wait until it’s too late. Start thinking about insurance today, and make sure you are adequately protected in case of the unexpected.

Read More: How to compare and choose the right health insurance plan for you and your family

Taming the Lifestyle Inflation Beast

A. The Perils of Spending Beyond Your Means

We all have dreams and aspirations of living our best life, but it’s important to make sure that our spending habits don’t spiral out of control. Living beyond your means can be a slippery slope that leads to financial instability and long-term debt.

B. Strategies for Keeping Lifestyle Inflation in Check

One of the best ways to avoid lifestyle inflation is to create and stick to a budget. This will give you a clear picture of your income and expenses and help you make informed decisions about your spending. Another helpful strategy is to save a portion of each pay raise or bonus, instead of using it all to increase your lifestyle. And, perhaps most importantly, being mindful and intentional about your spending can help you resist the temptation to keep up with the Joneses.

C. The Consequences of Lifestyle Inflation

Lifestyle inflation can lead to financial stress and debt. If you’re constantly spending more than you earn, it can be difficult to build an emergency fund, pay off debt, or save for your future. In the long run, it can also impact your ability to retire comfortably or reach other financial goals. So, it’s crucial to keep your spending in check and avoid the pitfalls of lifestyle inflation.

Save for Short-term Goals: The Key to Reaching Your Dreams Sooner Than Later

A. Why Saving for Short-term Goals is a Must

Saving for short-term goals is just as important as saving for retirement or paying off debt. It helps you stay on track and achieve your financial goals faster. Whether it’s a down payment for a home, a new car, or a dream vacation, having short-term savings can make a huge difference in how quickly you can reach your goals.

B. Setting and Achieving Financial Goals: A Step-by-Step Guide

To start saving for short-term goals, the first step is to set your goals. Decide what you want to achieve, and then determine how much you need to save each month to reach your goal. Setting up a dedicated savings account for each goal can help you stay on track and avoid dipping into your savings for other expenses.

C. The Role of Savings in Financial Success

Saving for short-term goals is not just about reaching your goals faster, it’s also about building good financial habits. By setting and achieving financial goals, you’re developing a mindset of financial responsibility and discipline. This mindset will serve you well in the future, as you continue to save for bigger goals and strive for financial stability. So, make sure to include saving for short-term goals as a key component of your financial plan.

D. Networking is Key to Career and Earning Potential

We all know that the right connections can go a long way in helping you reach your career and financial goals. But, it can be difficult to know where to start building your professional network. The good news is, it’s never too early (or late) to start making connections. Here are some tips to get you started.

E. Making the Right Connections

Networking isn’t just about handing out business cards at a networking event. It’s about making meaningful connections with people who can help you achieve your career and financial goals. This can be done through a variety of methods, such as attending professional events, reaching out to industry leaders, or even connecting with friends and family members in your desired field.

F. Building Relationships

Once you’ve made a connection, it’s important to nurture that relationship. This means following up with the person, offering to help them in any way you can, and staying in touch. Remember, networking is a two-way street. The more you help others, the more they’ll be willing to help you in return.

G. The Benefits of Professional Connections

Having a strong network of professional connections can have a major impact on your career and earning potential. For example, they may be able to introduce you to job opportunities, offer advice and mentorship, and provide valuable industry insights. So, don’t be afraid to put yourself out there and start making connections.

Read More: 10 Simple Tips for Saving Money on a Tight Budget

Seek Financial Advice: Get a Pro in Your Corner

It’s no secret that money can be confusing, especially when it comes to making the right moves for your future. That’s why seeking out financial advice is one of the smartest money moves you can make in your 20s. Not only can it help you avoid costly mistakes, but it can also give you peace of mind knowing that your financial future is in good hands.

A. Why Seek Financial Advice?

The benefits of seeking financial advice are many, but perhaps the most important is that it provides you with a professional and objective perspective on your finances. A financial advisor or planner can help you create a comprehensive financial plan that takes into account your current financial situation, your short- and long-term goals, and the best strategies for achieving those goals.

B. Options for Financial Advice

When it comes to seeking financial advice, there are plenty of options available. You can work with a financial advisor or planner, or you can take advantage of online resources like financial calculators and budgeting tools. Whichever route you choose, the key is to make sure you find a professional you trust and feel comfortable working with.

C. The Role of Financial Advice in Financial Success

Having a solid financial plan in place is crucial for financial success, and seeking out financial advice can help you achieve that success. Whether you’re saving for retirement, paying off debt, or investing, having a professional in your corner can help you make the right moves to achieve your financial goals and secure your financial future. So don’t be afraid to seek out the help of a financial advisor or planner – it could be one of the smartest money moves you make in your 20s.

Tax-Smart Money Moves: The Importance of Being Mindful of Taxes

Everyone knows that taxes are a necessary evil, but did you know that being mindful of taxes can actually have a huge impact on your financial stability? Understanding tax laws and regulations, as well as implementing strategies to minimize your taxes and maximize your refunds, can be game-changers when it comes to achieving financial success in your 20s.

A. Understanding Tax Laws and Regulations

The tax code is complex, and it’s easy to get overwhelmed with all the rules and regulations. But understanding the basics of how taxes work, including your tax bracket and deductible expenses, is key to making informed decisions about your finances. Take the time to educate yourself on tax laws and regulations, and don’t be afraid to reach out to a professional for help if you need it.

B. Strategies for Minimizing Taxes and Maximizing Refunds

There are many strategies for minimizing your tax liability and maximizing your refund, such as contributing to a 401(k) plan or taking advantage of tax credits. Additionally, taking the time to plan your finances strategically throughout the year can help you avoid costly mistakes and reduce your tax liability. Be mindful of the deadlines for tax-related tasks, and consider working with a professional to ensure you’re making the most of all your tax benefits.

C. The Impact of Taxes on Financial Stability

Taxes can have a big impact on your financial stability, and being mindful of taxes can help you avoid costly mistakes and make smart financial decisions. By understanding the tax laws and regulations, implementing strategies to minimize your taxes, and seeking advice from a professional if necessary, you can ensure that taxes don’t hold you back from achieving your financial goals.

Summing Up Your Money Moves: A Recap of the 15 Smartest Financial Decisions for Your 20s

A. Recap of the 15 Smartest Money Moves

In this article, we’ve explored the 15 smartest money moves to help you achieve financial success in your 20s. From paying off debt, creating a budget, saving for retirement, investing in your education, starting to invest, building good credit, purchasing insurance, avoiding lifestyle inflation, saving for short-term goals, networking and building professional connections, seeking financial advice, being mindful of taxes, and more, we’ve covered a wide range of topics to help you set a solid financial foundation for the future.

B. The Importance of Financial Planning and Preparation

Financial planning and preparation are key to achieving financial success. By taking the time to understand your financial situation and make smart money moves, you’ll set yourself up for a brighter financial future. By following these tips and strategies, you’ll be well on your way to achieving your financial goals and building a successful financial future.

C. Final Thoughts on Financial Success in Your 20s

Your 20s is a crucial time in your life to start building a solid financial foundation. By making smart money moves and being proactive about your finances, you’ll set yourself up for a bright financial future. So don’t wait, start today and make the most of your 20s.

Remember, financial success is a marathon, not a sprint. It takes time and effort, but with persistence and determination, you’ll get there. Good luck on your financial journey!

Frequently Asked Questions

Q: What are money moves?

A: Money moves are financial decisions or actions you take to improve your financial situation, such as creating a budget, saving for retirement, investing, building good credit, purchasing insurance, avoiding lifestyle inflation, saving for short-term goals, networking, seeking financial advice, being mindful of taxes, and more.

Q: What are some other ways to achieve financial success besides the money moves mentioned in the article?

A: While the 13 money moves listed in the article are a great starting point for achieving financial success, there are many other strategies to consider. These may include finding ways to increase your income, creating an emergency fund, reducing debt, creating a long-term financial plan, and seeking out resources such as books, online resources, or professional help.

Q: What is the best way to stick to a budget and save money?

A: The best way to stick to a budget and save money is to make it a priority. This means tracking your spending, setting realistic financial goals, and avoiding lifestyle inflation. It is also important to have a solid understanding of your income and expenses, and to make saving a consistent part of your financial routine.

Q: Is it possible to achieve financial success without a high income?

A: Yes, it is possible to achieve financial success without a high income. In fact, many people with high incomes struggle with money management and debt. The key to financial success is creating a budget, reducing debt, saving and investing regularly, and seeking out financial advice as needed.

Q: How can I stay motivated to achieve my financial goals?

A: Staying motivated to achieve your financial goals can be a challenge, but there are several strategies that can help. These may include setting achievable goals, breaking down large goals into smaller, more manageable steps, and celebrating small victories along the way. Surrounding yourself with a supportive community, seeking out accountability partners, and tracking your progress can also be helpful.

Q: What is the biggest mistake people make when it comes to their finances?

A: The biggest mistake people make when it comes to their finances is often not taking the time to understand and manage their money. This may include neglecting to track their spending, not saving regularly, or failing to seek out financial advice when needed. It is important to take the time to understand your financial situation and to make a plan for your money that aligns with your goals and values.

Q: Can money moves help me become financially independent?

A: Yes, making smart financial decisions and following through on them can help you achieve financial independence. Building wealth over time, avoiding debt, and having a solid financial plan are all steps towards financial independence.

Q: Is it too late to start making money moves if I’m in my 30s or 40s?

A: No, it’s never too late to start making smart financial decisions. While it’s ideal to start as early as possible, making positive financial changes at any stage of life can have a significant impact on your financial future.

{kind=link}